Iran’s strategic behavior has evolved into a systemic threat to the global economy, driven by its disruption of energy flows, critical maritime chokepoints, and key infrastructure. These actions have not only increased global uncertainty, but have also triggered higher supply chain costs, energy price volatility, and sustained inflationary pressures.

The European Institute for Peace and Governance (EIPG)

In the contemporary global economy, geopolitical risks are no longer measured solely by their ability to trigger direct military conflict, but increasingly by their capacity to disrupt trade and energy flows and raise the cost of economic stability. Within this context, Iran has emerged as a key source of systemic risk, driven by a strategic approach that leverages security tensions as a tool of economic influence.

In recent years, Iranian policies have become closely associated with disruptions in critical maritime corridors, particularly in the Arabian Gulf and the Red Sea, two of the world’s most vital arteries for trade and energy. Attacks on oil tankers and commercial vessels, whether carried out directly or through Iran-linked actors, have led to significant increases in shipping and insurance costs, as well as partial disruptions to global trade flows, with direct repercussions for global supply chains.

At the same time, the scope of these threats has expanded to include the targeting of critical infrastructure in Gulf countries, including oil facilities and airports, through missile and drone attacks. Iran-linked networks such as the Houthis in Yemen and militias in Iraq and Lebanon have played a central role in extending these threats beyond Iran’s borders, transforming them from instruments of regional influence into sources of cross-border economic pressure.

This growing intersection between security and economics reflects a broader shift in Iran’s role from a regional actor seeking to expand influence to one that directly impacts the stability of global markets, particularly in the energy and trade sectors. Rather than remaining confined within a limited geopolitical scope, these policies have become a persistent factor in shaping global economic risk dynamics.

In this context, energy expert Daniel Yergin notes that: “It is no longer possible to treat Iranian behavior as an isolated regional issue, but rather as a factor that directly affects the structure of the global economy. This behavior has increased the cost of trade and reshaped investment decisions in regions linked to critical maritime corridors.”

Accordingly, this study aims to examine how Iranian behavior, particularly the use of indirect threats through maritime routes and critical infrastructure affects global economic security, as well as the stability of energy markets and supply chains.

The risk posed by Iranian policies lies in their ability not to generate a single isolated crisis, but to contribute to the accumulation of interconnected systemic risks. Disruptions in maritime routes lead to higher shipping costs, which in turn drive up the prices of goods, fuel inflation, and impact financial stability across multiple economies. This interaction reflects what is known as “cascading risks,” where shocks rapidly spread from one sector to another. According to World Bank analyses, the global economy has become increasingly vulnerable to such risks due to the deep interdependence of supply chains and energy systems.

The figure illustrates the geographic spread of attacks on oil tankers and critical infrastructure across the Gulf, the Gulf of Oman, and the Red Sea, highlighting their transformation into a persistent threat to energy security. It also underscores the limited capacity of alternative routes, such as pipelines, to compensate for flows through the Strait of Hormuz, revealing the structural vulnerability of the global energy system.

Threats to Maritime Routes: From Strategic Pressure Tools to Global Economic Disruption

Maritime routes in the Arabian Gulf and the Red Sea constitute a fundamental pillar of the global economy, as a significant share of international trade and energy supplies passes through them. In this context, these corridors have increasingly become zones of rising tension in recent years, driven by Iranian behavior that relies on indirect threats as a strategic tool of pressure. This approach has contributed to an unprecedented increase in global economic risk levels.

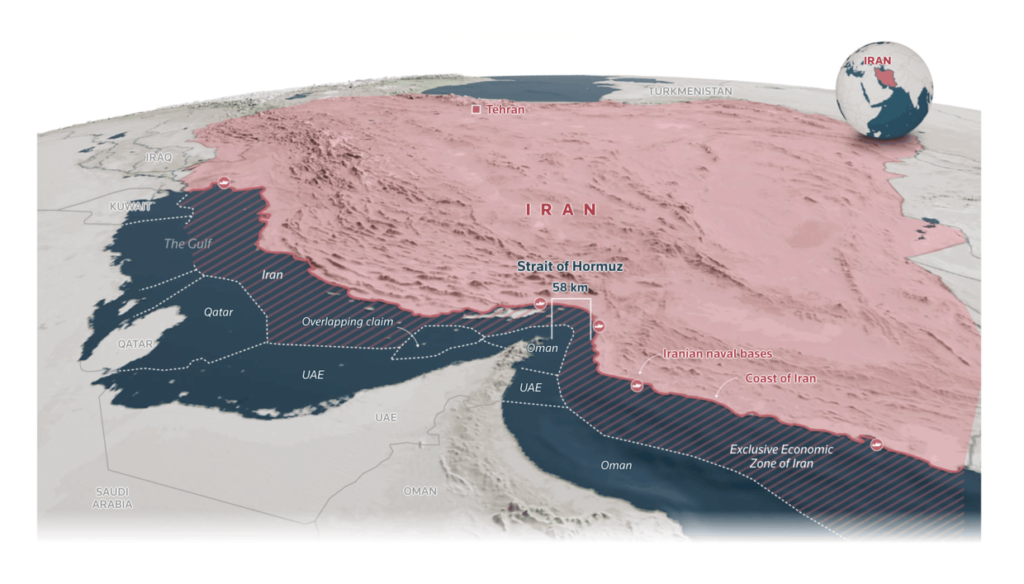

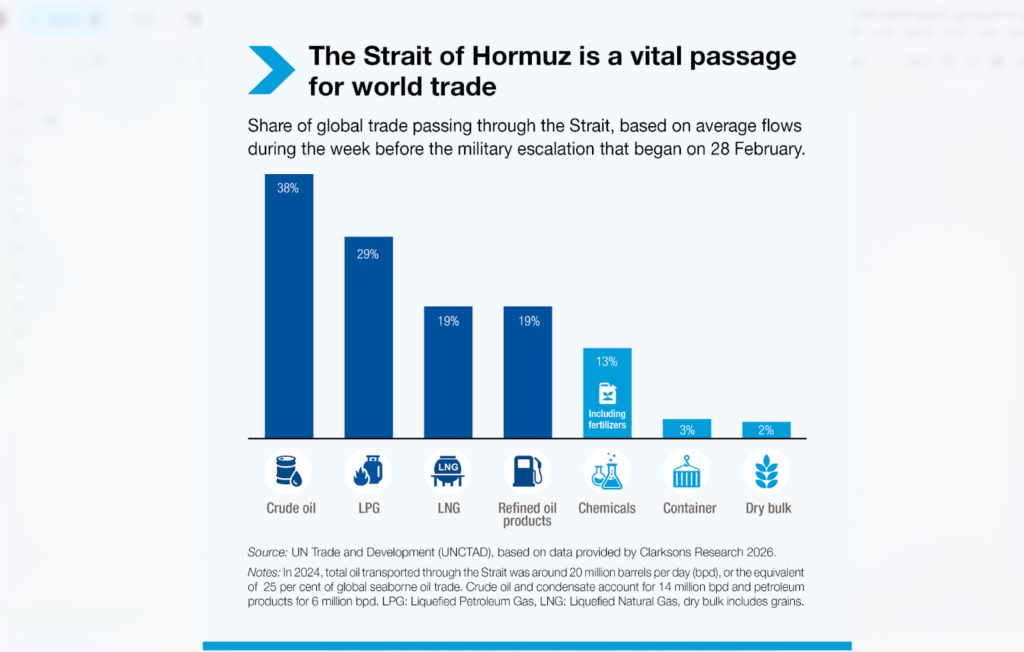

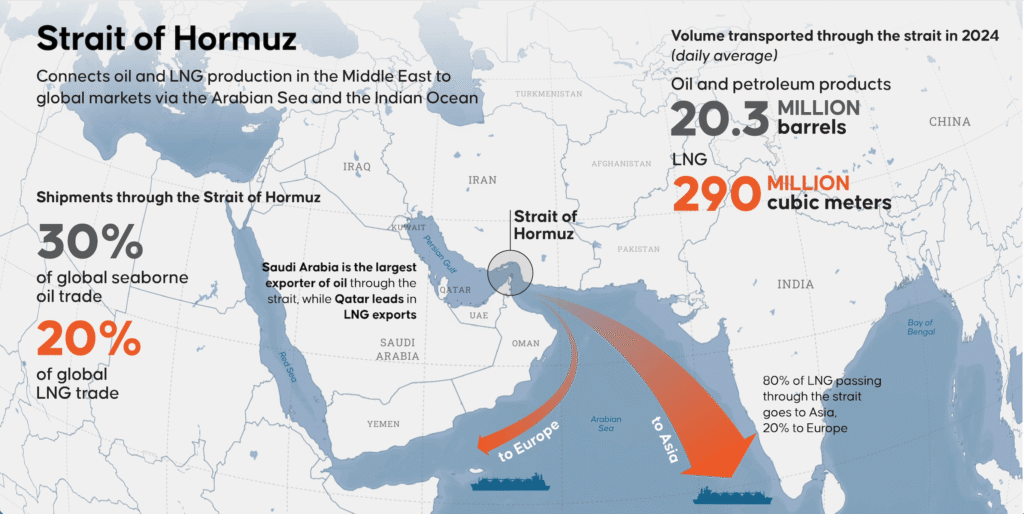

The Strait of Hormuz represents the most critical chokepoint in this system, with approximately 20% of global oil supplies passing through it, alongside substantial volumes of liquefied natural gas.

The Strait of Hormuz is one of the world’s most critical maritime chokepoints, through which roughly a quarter of globally seaborne oil trade passes, in addition to significant volumes of liquefied natural gas and fertilizers.

This geographic position gives Iran significant leverage over global markets, not only through production, but also through the ability to threaten the flow of energy supplies. According to analyses by the International Energy Agency (IEA), any disruption in this chokepoint leads to immediate volatility in oil prices and heightened uncertainty in global markets.

Rough estimates suggest that a closure of the Strait of Hormuz could reduce global oil flows by approximately 11 million barrels per day, even after accounting for partial mitigation through stock releases or alternative routes. Compared to pre-crisis demand levels, this would result in a supply deficit of around 9 million barrels per day, a substantial shortfall exceeding the combined oil consumption of the United Kingdom, France, Germany, Spain, and Italy.

The situation is even more acute in the liquefied natural gas (LNG) sector. The Strait of Hormuz typically accounts for about 20% of global LNG supplies, with shipments from the Middle East playing a critical role in meeting global demand. Unlike oil, there are no viable alternative routes for transporting LNG at scale, and strategic reserves are limited, making the market particularly vulnerable to disruptions.

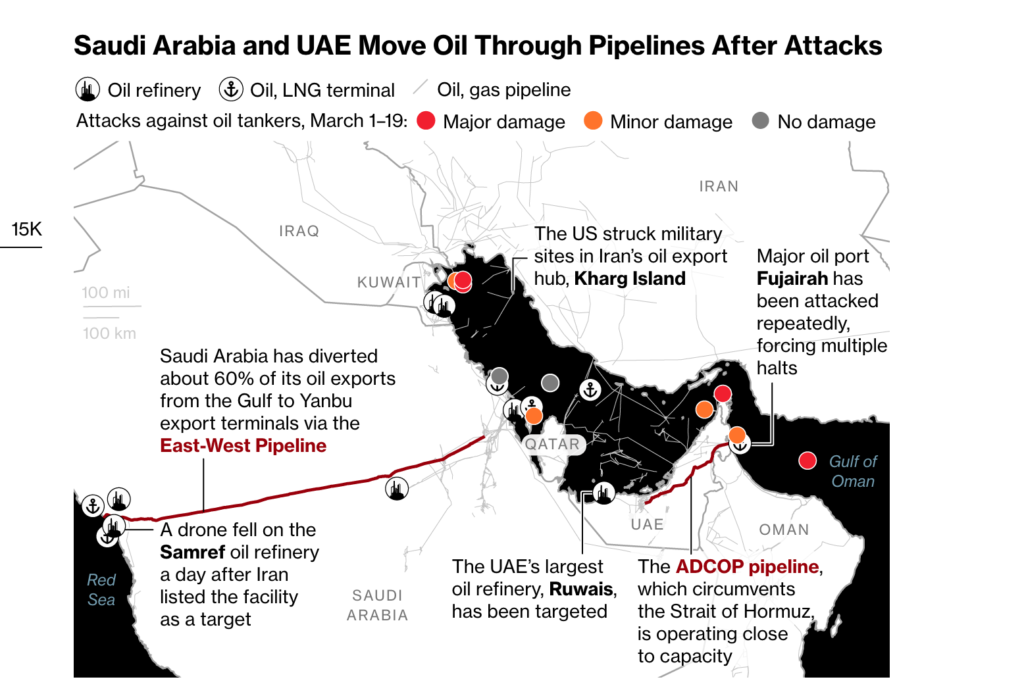

These threats have not remained rhetorical; they have materialized in a series of incidents targeting oil tankers and commercial vessels in the Gulf, the Gulf of Oman, and the Red Sea either directly or through Iran-linked actors. This pattern of attacks has led to a significant increase in maritime insurance costs, with premiums rising by 30–50% in some periods for vessels transiting high-risk zones. Such increases are not merely additional costs, but are quickly passed on to global markets through higher energy and commodity prices.

In this context, energy expert Daniel Yergin notes: “Any threat to maritime routes in the Gulf does not remain regional in impact; it immediately transmits to global markets through prices and supply chains.”

Moreover, escalating tensions in the Red Sea particularly through attacks carried out by the Iran-backed Houthi group have expanded the scope of the threat to include one of the world’s most critical trade routes, linking Asia to Europe via the Suez Canal.

This figure illustrates the extent of global dependence on the Strait of Hormuz, through which approximately 20% of global energy supplies pass, making any threat to it directly impactful on the international economy.

These escalating threats have forced many global shipping companies to reroute their vessels around the Cape of Good Hope, significantly increasing transit times and shipping costs, while creating bottlenecks across global supply chains.

According to estimates by international shipping institutions, diverting routes away from the Red Sea can extend voyage durations by approximately 10 to 15 days, and increase transportation costs by up to 40% in some cases.

These rising costs do not remain confined to the transport sector; they are ultimately passed on to end consumers through higher prices of goods, thereby intensifying global inflationary pressures.

From a strategic perspective, this pattern reflects a shift in Iran’s tools of influence from direct engagement to the use of critical maritime chokepoints as a form of indirect leverage. However, while such a strategy may generate short-term disruption, it simultaneously reinforces Iran’s classification as a source of systemic risk to global economic stability, prompting international actors to strengthen deterrence and containment policies.

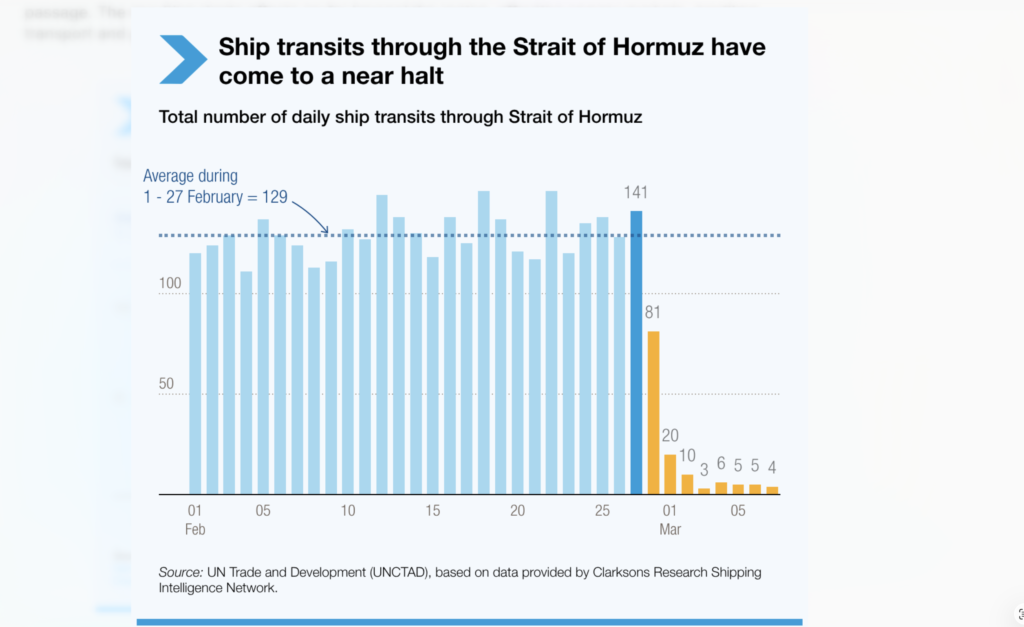

The figure illustrates a near-total disruption of vessel traffic through the Strait of Hormuz as a result of Iranian attacks, along with the total number of ships that typically transit the strait on a daily basis.

In this context, maritime security expert Elena Studdard notes: “Using maritime corridors as a tool of pressure may deliver tactical gains, but it raises the strategic cost of confrontation and deepens the isolation of the state employing it.”

Based on this, it can be argued that the true cost of such behavior extends beyond direct damage, encompassing the reshaping of global trade patterns and the elevation of systemic risk within the international economy.

As these threats persist, maritime corridors are no longer merely channels of commerce, but become enduring flashpoints of tension, reflecting a growing imbalance between security and economic stability.

Attacks on Gulf States: Targeting Infrastructure and Turning the Economy into a Battlefield

Threats associated with Iran are no longer confined to the maritime domain or indirect pressure tactics. In recent years, they have evolved to include direct targeting of critical infrastructure in Gulf countries, including oil facilities, airports, and energy hubs.

This shift reflects a transition from limited pressure tactics to a strategy aimed at generating direct economic impact, one that affects not only the targeted states but also reverberates across global markets.

These dynamics became particularly evident in attacks on major oil facilities in the region, which in some cases led to the temporary disruption of a significant share of oil production. Estimates suggest that large-scale targeting of Gulf energy infrastructure can trigger immediate disruptions in global supply, given the central role the region plays in international energy markets.

The nature of these attacks has also evolved in terms of tools and technologies, with increasing reliance on drones and missile systems, making them more difficult to detect and intercept. This technological shift has not only enhanced the effectiveness of such operations but has also expanded their geographical scope to include civilian and economic targets, such as airports and key infrastructure.

In this context, regional security expert Jack Barry notes: “The shift toward targeting economic infrastructure reflects a growing recognition of the economy as a battlefield, not merely a byproduct of conflict.”

At the same time, Iran-aligned groups, most notably the Houthis in Yemen, have played a central role in carrying out these attacks, providing Tehran with a degree of political deniability while maintaining strategic impact. This model of proxy warfare does not reduce the scale of the threat; rather, it increases its complexity, blurring lines of responsibility while leaving tangible economic consequences.

From an economic perspective, this escalation has significantly raised investment risk levels in the region, as international companies increasingly factor in the likelihood of infrastructure targeting when making strategic decisions. Insurance costs for critical assets have risen, and defense spending has increased, placing an additional burden on regional economies.

In this context, Middle East expert Fawaz Gerges argues that: “Targeting infrastructure in the Gulf is not merely about inflicting direct damage, but about reshaping the region’s economic security environment in a way that increases the cost of stability.”

Accordingly, attacks on Gulf states can be understood as an advanced phase in Iran’s strategic approach, where the economy itself is used as a battlefield. However, while this strategy may generate short-term effects, it simultaneously contributes to the strengthening of counter-regional alignments and increased security coordination, ultimately limiting its long-term effectiveness and amplifying its strategic cost.

The impact of energy disruptions is not limited to the oil and gas sector; it extends directly to global food security. Rising energy prices increase the cost of agricultural production and transportation, which in turn drives up food prices. Moreover, Gulf countries are among the world’s leading exporters of fertilizers, a sector heavily dependent on natural gas.

As a result, any disruption to energy flows through critical chokepoints affects fertilizer production and exports, posing risks to food security in import-dependent regions, particularly in Africa and Asia. This interconnected dynamic makes Iran-related tensions an indirect but significant driver of global food insecurity.

Energy and Global Markets: From Tension to Disruption of the International Economy

Energy is no longer merely an economic sector; it has become one of the key determinants of stability in the international system. The security of oil and gas supplies is now directly linked to global market dynamics, inflation, and economic growth. In this context, Iran plays a pivotal role in shaping this stability not only as an energy producer, but as a geopolitical actor capable of influencing its flow.

Moreover, the impact of Iranian escalation is not limited to energy prices alone; it extends to global supply chains. Rising shipping and insurance costs increase the cost of transporting goods, which in turn raises prices in global markets. This dynamic intensifies inflationary pressures, particularly in energy-importing economies.

Ongoing threats in the Gulf and the Red Sea have also compelled many companies to reassess their logistics strategies and seek safer—albeit more costly alternative routes. This shift affects not only costs but also the efficiency of global trade, as delays increase and port congestion intensifies, creating cascading effects across multiple sectors.

The danger of Iran’s behavior lies in the fact that it does not merely threaten a regional corridor, but rather one of the central arteries of the global economy. According to the U.S. Energy Information Administration, oil flows through the Strait of Hormuz reached approximately 20 million barrels per day in 2024—equivalent to around 20% of global petroleum liquids consumption—while roughly 20% of global liquefied natural gas trade also passed through the strait. This means that any escalation in this chokepoint affects not only oil prices, but global energy security as a whole.

Analyses by the World Bank further indicate that energy disruptions represent one of the most significant sources of risk to the global economy, particularly given the deep interconnection between geopolitical crises and supply chains. Within this framework, Iran-related tensions act as a risk multiplier, rather than a standalone variable.

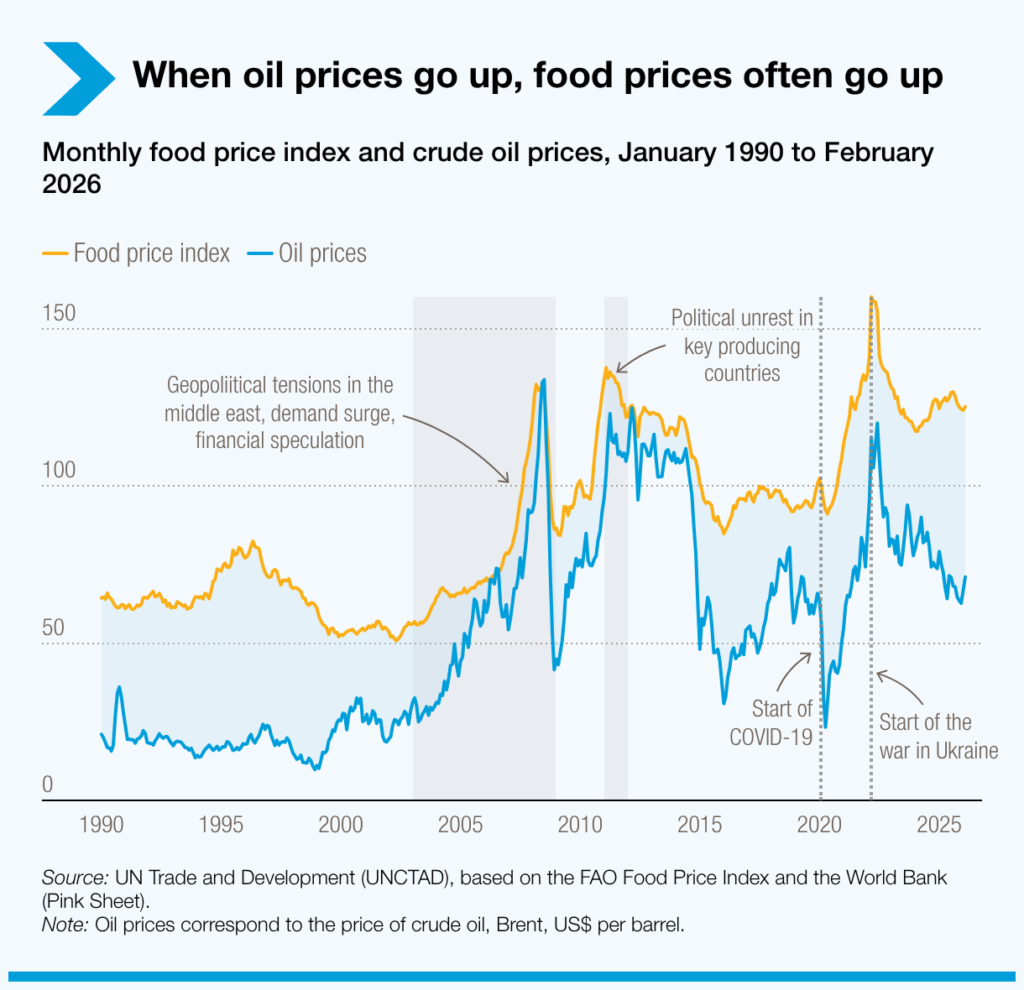

When oil prices rise, food prices tend to increase as well. Monthly Food Price Index and Crude Oil Prices, January 1990 – February 2026.

On the other hand, this reality leads to a decline in long-term investments in the energy sector, particularly in high-risk regions, where companies hesitate to commit capital in an unstable environment. This hesitation affects the market’s ability to meet future demand, increasing the likelihood of energy crises in the medium term.

In this context, international economics researcher Sarah Moulney notes:

“Iran-related tensions do not only affect the present; they reshape investment decisions in the energy sector, creating long-term impacts on markets.”

Accordingly, Iran’s role in global energy markets extends beyond production and export; it increasingly influences how risk is priced within international markets. Rather than serving as a stabilizing force, Iran has become a factor that heightens uncertainty, increases price volatility, and shapes investment and trade decisions.

At the same time, Iran’s own economic indicators reflect a growing fragility in its ability to absorb the external costs of its policies. According to International Monetary Fund estimates, inflation reached 41.6%, while the World Bank estimated economic growth in 2024 at only 3.7%, a level insufficient to ease social pressures or restore investor confidence. Iran’s GDP stood at approximately $475.25 billion, indicating that the economy continues to operate under constraints imposed by sanctions, declining investment, and persistent political risk.

This shift reflects a structural imbalance, where geopolitical tools are used to achieve short-term gains at the expense of broader economic stability ultimately raising the cost for all actors involved, including Iran itself.

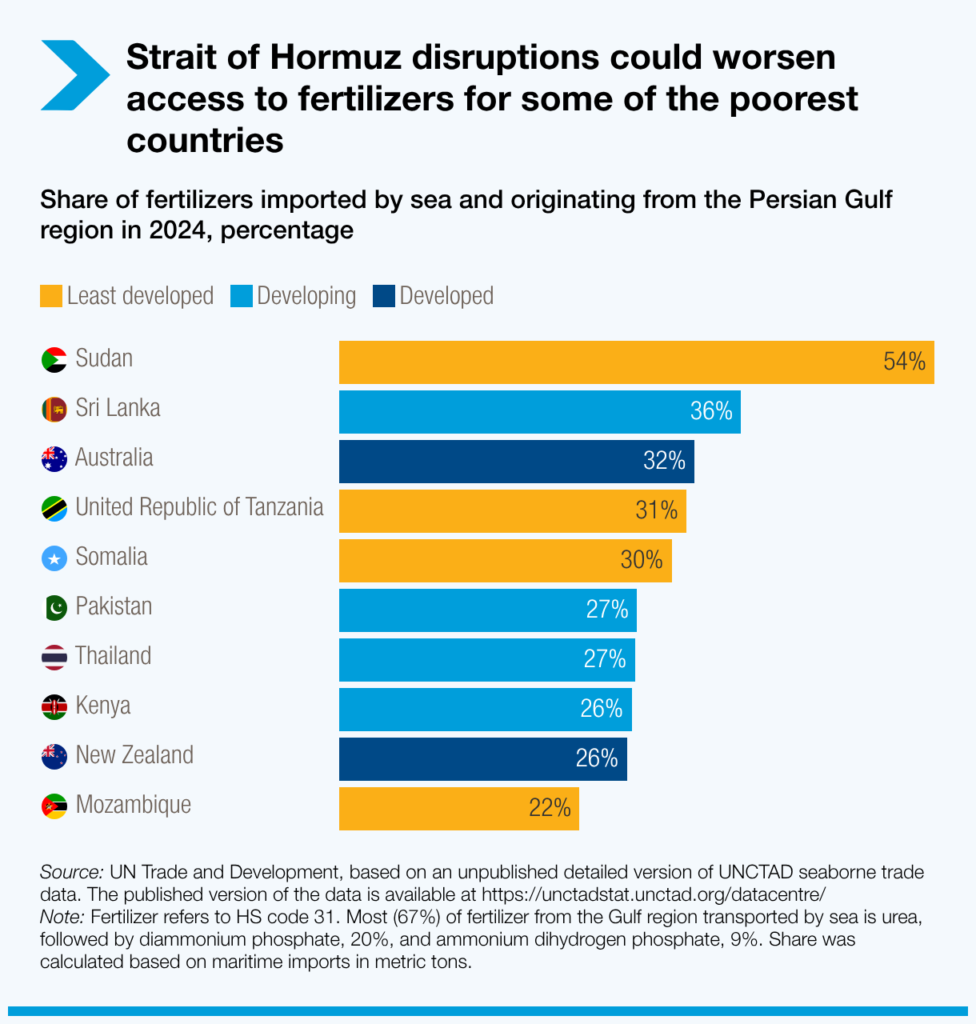

Disruptions in the Strait of Hormuz exacerbate the difficulty for some of the world’s poorest countries to access fertilizers.

Share of seaborne fertilizer imports originating from the Arabian Gulf region in 2024 (percentage).

Militias and Proxy Networks: Expanding the Threat and Turning Influence into a Strategic Liability

Iran’s use of militias and transnational armed networks represents a defining feature of its regional strategy. Tehran has relied on these instruments to expand its influence without direct engagement in confrontation. However, this model, while enabling rapid expansion has gradually evolved into a broad source of instability, extending beyond the security domain to impact both regional and global economies.

These networks include key actors such as the Houthis in Yemen, militias in Iraq, and Hezbollah in Lebanon. Operating as indirect extensions of Iranian policy while retaining a degree of operational autonomy, they allow Iran to exert influence across multiple theaters simultaneously. Yet this model also expands the scope of risk and makes the consequences of such policies increasingly difficult to control.

In this context, Middle East expert Dr. Carlos Vique notes:

“Iran’s reliance on proxies provides broad influence at a lower direct cost, but it creates an unstable environment whose long-term outcomes are difficult to control.”

Economically, these militias have played a direct role in targeting critical infrastructure ranging from attacks on oil facilities in the Gulf to threats against maritime navigation in the Red Sea, as well as strikes on military bases and airports. These operations have not only caused material damage, but have also contributed to rising insurance costs, reduced investment, and heightened operational risks across the region.

Moreover, this pattern of indirect threat has significantly expanded uncertainty. Risks are no longer confined to a single state, but are distributed across multiple theaters, complicating the ability of markets and businesses to anticipate and respond effectively. This diffusion of risk directly impacts the global economy through increased transportation and energy costs, as well as disruptions to supply chains.

At the same time, these networks have failed to generate political stability in the areas where they operate. Instead, they have weakened state institutions, deepened internal divisions, and transformed these countries into high-risk economic environments. This has resulted in declining foreign investment, rising unemployment, and increased reliance on informal economies.

Strategically, this model reveals a fundamental paradox: while Iran seeks to expand its influence through these instruments, it simultaneously contributes to the creation of a more hostile regional environment. This, in turn, leads to the formation of counter-alliances, increased deterrence measures, and a shrinking political margin of maneuver.

Furthermore, the growing reliance on militias reflects the limitations of traditional state tools, as diplomacy and economic engagement are increasingly replaced by unstable security-based approaches. Rather than enhancing power, this shift entrenches a model of influence that is high-risk and low in long-term sustainability.

Accordingly, militias can no longer be seen merely as instruments of influence; they have become a central factor in amplifying the strategic cost of Iranian policies, by expanding the scope of threats, deepening instability, and increasing economic risks at both regional and international levels.

As this approach persists, these networks are gradually transforming from sources of leverage into strategic liabilities constraining Iran’s ability to achieve long-term stability, increasing its isolation, and widening the gap between its regional ambitions and its actual capabilities.

Beyond military and security tools, Iran has also developed a parallel economic system that enables it to circumvent international sanctions and maintain steady financial flows. This system includes oil smuggling networks, front companies, and informal payment mechanisms relying on regional and international intermediaries.

Estimates suggest that Iran managed to export between 1.2 and 1.5 million barrels of oil per day through unofficial channels in 2024, despite ongoing sanctions. This parallel economy creates a non-transparent financial environment that facilitates the funding of activities outside formal frameworks, further complicating efforts to trace financial flows and assess their impact on regional economic stability.

Exporting Crises and Importing Costs

The findings of this study reveal a structural flaw in the strategic logic underpinning Iranian behavior. While Tehran relies on expansion-oriented tools aimed at increasing its influence, these approaches ultimately generate counterproductive effects that weaken this influence over the medium and long term.

This paradox lies in the fact that the use of militias, the disruption of critical maritime corridors, and the targeting of infrastructure provide Iran with relatively low direct-cost tools of influence. However, they significantly increase indirect costs through sanctions, isolation, and elevated economic risk.

In this sense, Iranian behavior cannot be viewed as a successful expansion strategy, but rather as a model marked by a disconnect between means and outcomes. As the scope of influence expands, economic pressures intensify, and the ability to capitalize on that influence diminishes creating a widening gap between strategic ambition and actual capacity.

This dynamic produces what can be described as a high-impact, low-return model, in which Iran achieves broad regional presence but fails to translate it into sustainable economic or political gains. Instead of strengthening its position, this presence complicates its strategic environment and increases its vulnerability.

The evidence analyzed in this study indicates that Iranian policies are no longer a source of strength, but have become a central driver of economic and security instability at both regional and international levels. Rather than converting tools of influence into strategic gains, they have raised risk levels, intensified pressure, and reduced room for maneuver.

These policies have effectively transformed Iran from an actor seeking to expand its influence into one increasingly perceived as a source of threat to the global economy, particularly in the domains of energy and critical maritime routes. This shift has not only weakened its international standing, but has also increased its isolation and tied it more closely to fragile and economically unstable networks.

At the same time, this strategy has imposed growing economic pressures domestically, undermining the country’s ability to achieve sustainable stability and reflecting a failure to balance external ambitions with internal capabilities.

Accordingly, Iran’s current behavior reflects a broader transformation in the nature of conflict from direct military confrontation to the use of the economy as a strategic tool of pressure. Rather than engaging in conventional warfare, critical infrastructure and strategic corridors are targeted to generate wide-ranging economic effects. While this approach may deliver short-term impact, it ultimately increases global risk levels and raises the likelihood of escalation and external intervention.